Analysis of the business situation of China's printing industry from January to June 2021

Time:2021-08-03 From:

From January to June 2021, enterprises above designated size in China's printing industry realized operating income, an increase of 18.8% year-on-year; realized total profits, an increase of 11.8% year-on-year. The gap between revenue growth and profit growth is gradually widening.

1. Overall trend analysis

In the first half of the year, China's GDP growth rate was 12.7%, with an average growth rate of 5.3% in two years. In terms of quarters, the year-on-year growth rate in the first quarter was 18.3%, and the two-year average growth rate was 5.0%; the second quarter growth rate was 7.9%, and the two-year average growth rate was 5.5%, 0.5 percentage points faster than the first quarter. Judging from relevant indicators, in the first half of the year, the freight volume of the whole society increased by 24.6% year-on-year, with an average increase of 7.2% in two years; the electricity consumption of the whole society increased by 16.2% year-on-year, with an average increase of 7.1% in two years. The overall economy showed a sustained recovery trend.

The industrial production also continued the momentum of continuous growth. In the first half of the year, the industrial added value of all industries (enterprises above designated size) increased by 15.9% year-on-year, with an average increase of 7.0% in two years. Judging from the growth rate of the month, in June, the industrial added value of all industries (enterprises above designated size) increased by 8.3% year-on-year, an increase of 0.56% from the previous month. The added value of 34 of the 41 major industries maintained year-on-year growth.

From January to June 2021, the industrial added value of the "printing and recording media reproduction industry" increased by 18.0% year-on-year, which was higher than the average level of 15.9% for all industries. Judging from the growth rate in June, the industrial added value growth rate of the printing industry was 12.2%, which was also higher than the average level of 8.3% for all industries.

2. Revenue and profit analysis

From January to June 2021, enterprises above designated size in the printing industry realized operating income, a year-on-year increase of 18.8%. During the same period, all enterprises above industrial scale achieved operating income, a year-on-year increase of 27.9%. The production and sales of the printing industry accelerated significantly compared with the same period last year, but the growth rate was lower than the national industrial average.

From January to June 2021, enterprises above designated size in the printing industry realized total profits, a year-on-year increase of 11.8%. During the same period, the total profits of all enterprises above the industrial scale increased by 66.9% year-on-year, and the average increase in two years was 20.6%. Among the 41 major industries, 39 industries achieved a year-on-year increase in total profit. In the paper industry, which is closely related to the printing industry, the total profit from January to June increased by 77.1% year-on-year, compared with the 11.8% of the printing industry, which is quite different.

Comparing the change track of the growth rate of operating income and total profit of the printing industry this year, it can be seen that the growth rate of total profit has been greatly reduced. It was higher than the growth rate of operating income at the beginning of the year and began to be lower than the growth rate of operating income in May. Then in June, the gap with the revenue growth rate widened, showing that the profits of printing companies above the designated size were under pressure, and they continued to be impacted by factors such as rising commodity prices.

3. Benefit status analysis

In June 2021, the loss ratio of enterprises above designated size in the printing industry was 21.8%. Compared with 21.6% in the previous month, it has increased by 0.2 percentage points, showing that the loss has reached the bottom of the stage. However, it should be noted that this valley (21.8%) has increased a lot compared to 13.4% in 2019; and compared with 16.3% at the end of 2020, it has also increased by more than 5 percentage points. In the year when the printing industry is struggling to get rid of the impact of the epidemic and continues to recover, the differentiation of the industry is intensifying, and printing companies are facing a more severe test of life and death.

From January to June 2021, the operating income profit margin of the printing industry is 5.21%. It can be seen from Figure 4 that the profit margin of operating income has decreased compared with the previous month, and compared with 6.43% for the whole of last year, it has dropped by 1.22 percentage points. Compared with the average level of 7.11% in all industries from January to June, there is also a big gap. Prices of paper and other raw materials have risen several times this year, seriously eroding the profit margins of printing companies.

From January to June 2021, the cost per 100 yuan of operating income in the printing industry was 84.48 yuan, which was basically the same as that of the previous few months. This indicator is higher than the average level of 83.54 yuan for all industries.

4. Asset quality analysis

At the end of June 2021, the asset-liability ratio of enterprises above designated size in the printing industry was 46.40%. Compared with the previous month's 46.17% debt ratio, a slight increase. Compared with the 56.5% asset-liability ratio of all industries at the end of June, the debt level of printing companies is generally low.

At the end of June, the average payback period of accounts receivable of enterprises above designated size in the printing industry was 56.01 days. Compared with the end of last month, it has dropped by 1.2 days. However, compared with the average payback period of 51.4 days for all industrial accounts receivable at the end of June, the financial pressure of printing companies is still relatively large.

At the end of June, the inventory turnover days of finished products of enterprises above designated size in the printing industry were 17.86 days, a decrease of 0.38 days compared with the end of last month, and the inventory turnover speed continued to accelerate.

5. Analysis of export delivery value

From January to June 2021, the export delivery value of the printing industry increased by 8.6% year-on-year. Compared with the 22.9% export growth rate of the entire industry, the export growth of the printing industry recovered slowly. In June, the export delivery value of the printing industry increased by 5.9% year-on-year, compared with 5.4% in the previous month, and the growth rate picked up.

6. Price index analysis

Since January 2019, the pulp price index has experienced a period of decline, bottoming out, and slow climb during the epidemic period, and has entered a period of rapid increase, and it still rose strongly in June. The price index of papermaking is affected by the price index of pulp, the change rhythm is consistent, and it is also in a period of continuous rise. However, since June, the increase in its price index has begun to slow down.

In contrast, the ex-factory price index of printing industry producers and the price index of bookbinding and printing-related services were flat, which could not offset the cost increase brought about by the sharp increase in paper prices.

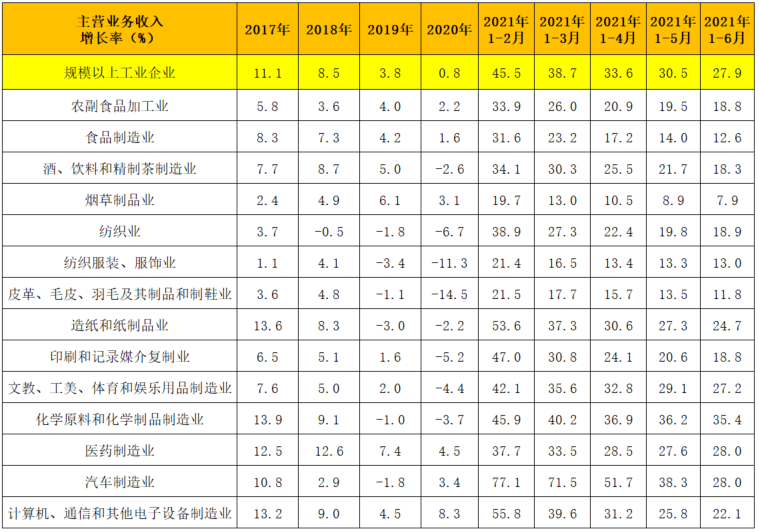

7. Trend analysis of some industries

Table 1 shows the growth of main business income of some industries closely related to the printing industry among the 41 major industries. Most of these industries are the customer industries served by the printing industry, and there are also upstream industries such as papermaking.

The table shows that from January to June 2021, the main business income of all industries increased by an average of 27.9%, which is in a continuous growth trend.

Table 1 Growth rate of main business income of some industries

The agricultural and sideline food processing industry, food manufacturing industry, wine, beverage and tea manufacturing industry and other industries related to people's livelihood are developing steadily; industries with high foreign trade dependence such as textile industry, clothing and apparel, leather fur and footwear industry are gradually recovering; affected by the new crown Due to factors such as production capacity expansion and output increase of vaccines, testing reagents and other epidemic prevention and anti-epidemic materials, the pharmaceutical manufacturing industry continues to grow rapidly; it is worth noting that due to the shortage of chips and some policy adjustment factors, the growth of the automobile industry has been restricted to a certain extent , the growth rate has been corrected; the growth rate correction has also spread to the electronics industry, but the correction is weaker than that of the automobile industry.

Overall, the national economy continued to recover steadily in the first half of the year. However, the economic recovery is still uneven, especially as rising raw material prices put pressure on the profits of mid- and downstream companies, and the recovery of profits is relatively slow. Printing companies still need to strengthen their confidence in development, enhance their development momentum, and strive to maintain healthy and sustainable development during the intertwined promotion period of economic recovery and industrial reshuffle.